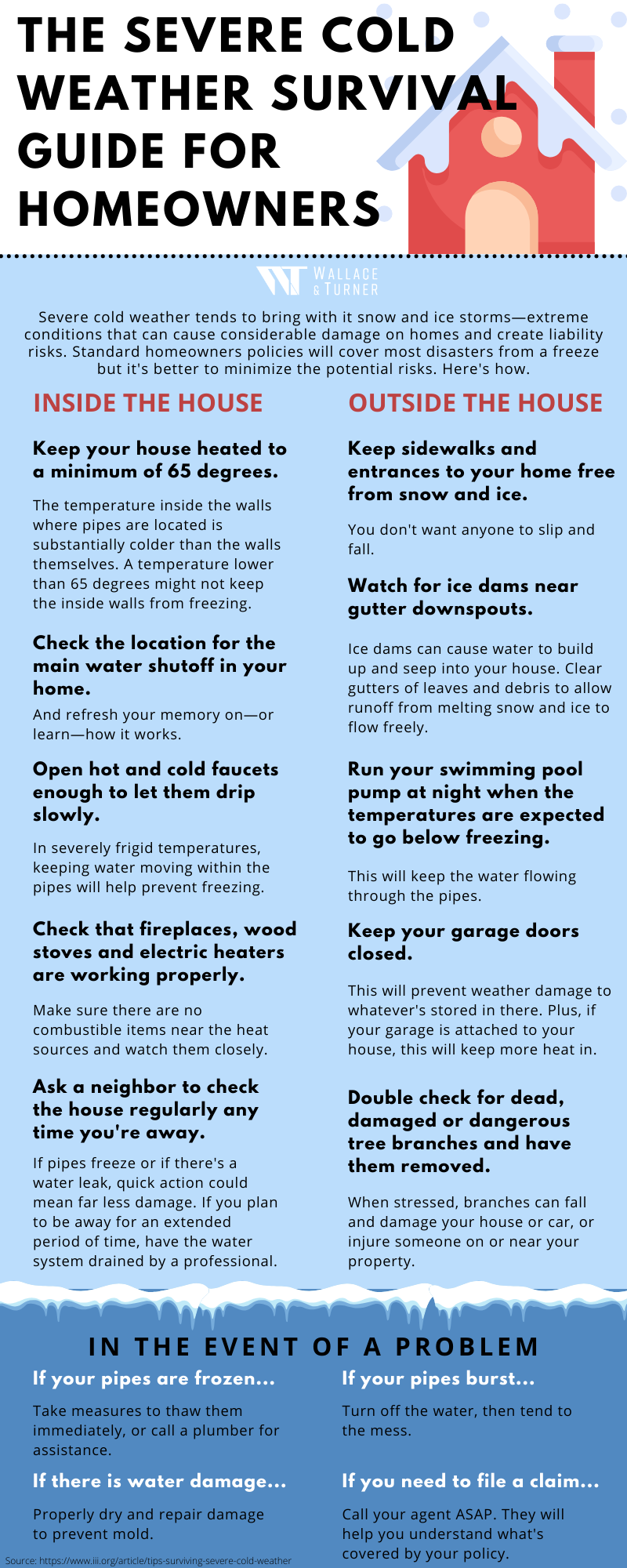

Ben Galbreath - Producer

Accidental death and dismemberment insurance is insurance coverage similar to that of life insurance, and is commonly used as a supplement to a life insurance policy. It covers an employee in the event of an accidental death, or an unforeseen accident that results in the loss or function of a body part (e.g., arms, legs, eyesight, speech, hearing). AD&D does not cover deaths caused by existing medical conditions.

Producer Ben Galbreath discusses what small businesses should know about accidental death & dismemberment insurance:

What is accidental death and dismemberment insurance (AD&D)?

Accidental Death & Dismemberment insurance is a good coverage to be added to a benefits portfolio. This coverage is on a very limited form, meaning it will only pay a benefit due to an accident. Definition of an “accident” is an unforeseen incident that happens unexpectedly and unintentionally. The coverage is triggered only by an accident.

Do you have to offer AD&D to employees?

AD&D is an optional benefit that can be added to an employer’s benefit portfolio. If the benefit is offered to one employee, it will need to be offered to all. The employees will have the option to take the coverage or not. An employer does not have to offer the AD&D if they don’t want to. If health coverage is offered, AD&D is usually a rider included on the coverage. It can also be offered individually.

How does offering AD&D to employees benefit employers?

Employers offering AD&D benefits is a way of broadening health benefits to make their business more attractive to prospective employees. With the growing struggle to recruit and retain quality employees, this could attract those employees.

How does being offered AD&D benefit employees?

The coverage benefits employees to some extent – if an employee has an accidental dismemberment, it would help with the medical bills and rehabilitation. In terms of accidental death, the death benefit would be paid out to the employee’s family.

What does AD&D cover?

AD&D is only triggered in the event of an accident, meaning unintentional death or dismemberment of the insured. Death is self-explanatory and the death benefit would be paid out. When it comes to dismemberment coverage, this would apply to loss, or the loss of use, of body parts or functions (e.g., limbs, speech, eyesight, hearing).

Anything else a small business owner should know about AD&D?

AD&D is usually added to a group health policy for a very minimal cost, but it can also be offered as standalone coverage. Additionally, AD&D can be added to a life policy or group life policy.

Small business owners need to be very careful when offering this coverage due to its limited coverage for unlikely events. It is supplemental life insurance and not an acceptable replacement for term or whole life insurance. This is why it’s usually added to group health or life coverage.

Generally speaking, I don’t advise small business owners to offer AD&D coverage on its own. This type of coverage can be offered in a better supplemental benefit programs. Many accident policies, critical illness and others, offer similar coverage. The best advice would be to speak with a supplemental benefits provider to understand the different options that are available. Working with an independent broker can help build a strong benefits package that could be more cost effective for the employer and employee.

Questions about AD&D insurance, or group health or life coverage? Contact Wallace & Turner at (937) 324-8492 in Springfield, (937) 652-8492 in Urbana, or info@wtins.com.